India’s mobility and infrastructure boom extends far beyond vehicle manufacturing. The real opportunity lies in the critical ground-level consumables, the commercial radials, Off-The-Road (OTR) heavy treads, and premium passenger tyres that keep the nation’s freight fleets rolling, agricultural machinery moving, and private vehicles glued to expanding expressways.

As logistics networks modernize, infrastructure spending accelerates, and consumer preferences shift toward higher-end and electric mobility, technologically superior tyre makers are capturing incremental market share from unorganized and lower-tier players. In this backdrop, JK Tyre & Industries Ltd. has entrenched itself as India’s undisputed pioneer in commercial radial technology with a rapidly growing high-margin consumer and EV tyre business.

But does JK Tyre & Industries Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | JKTYRE |

| Industry/Sector | Tyres & Allied |

| CMP | 410.00 |

| Market Cap (₹ Cr.) | 11,878 |

| P/E | 15.47 (Vs Industry P/E of 20.43) |

| 52 W High/Low | 611.90 / 311.00 |

| EPS (TTM) | 26.91 |

| Dividend Yield | 0.96% |

About JK Tyre & Industries Ltd.

JK Tyre & Industries Ltd. is one of India’s leading manufacturers of commercial, passenger, and specialized off-road tyres. The company operates primarily under the flagship JK Tyre brand and has established a commanding presence across the logistics, personal mobility, agricultural, and heavy infrastructure segments.

Over the decades, JK Tyre has evolved from a traditional commercial bias-tyre maker into a comprehensive mobility solutions provider, pioneering Truck and Bus Radial (TBR) technology in India while expanding its portfolio to include premium passenger radials, EV-specific treads, and connected “smart tyre” technologies. The company commands a deeply entrenched domestic distribution network, spearheaded by its exclusive Steel Wheels and Truck Wheels retail centers, alongside a steady, expanding international footprint across more than 100 countries.

Key business segments

JK Tyre & Industries Ltd. operates primarily in the following key business segments:

- Commercial Tyres (TBR & TBB): Flagship Truck & Bus Radials (market leaders) and bias tyres for heavy/light logistics fleets.

- Passenger & EV Mobility: Premium radials for cars, luxury SUVs (Ranger / Levitas), 2/3-wheelers, and dedicated EV tyres

- OTR & Agriculture: Heavy-duty, extreme-durability tyres for mining earthmovers, construction, and farm machinery.

- Exports Business: Global supply across 100+ countries, strongly anchored by their Mexican subsidiary (JK Tornel).

- Smart Tyres & Services: Treel TPMS sensors for digital fleet tracking and organized retreading centers.

Primary growth factors for JK Tyre & Industries Ltd.

JK Tyre & Industries Ltd. key growth drivers:

- Logistics & Highway Upcycle: Rapid expansion of India’s expressway network driving higher commercial fleet utilization and faster tyre replacement cycles.

- The Premiumization Wave: Shifting consumer demand toward higher-margin, large-rim SUV tyres (16-inch+) and advanced Truck Radials.

- EV & Smart Mobility Push: Scaling up higher-margin, dedicated Electric Vehicle (EV) tyres and digital fleet management (Treel TPMS) solutions.

- Infrastructure & Mining Capex: Sustained government spending on mega-infrastructure and mining fueling solid demand for heavy Off-The-Road (OTR) treads.

- Export Market Penetration: Capitalizing on ‘China-Plus-One’ supply chain shifts to aggressively scale exports across North America, LATAM, and the Middle East.

Detailed competition analysis for JK Tyre & Industries Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| JK Tyres & Industries Ltd. | 16326.65 | 2031.37 | 12.44% | 774.19 | 4.74% | 15.47 |

| MRF Ltd. | 31149.01 | 4900.58 | 15.73% | 2426.10 | 7.79% | 23.07 |

| Balkrishna Industries Ltd. | 10823.08 | 2300.43 | 21.25% | 1243.10 | 11.49% | 34.66 |

| Apollo Tyres Ltd. | 28470.60 | 4143.23 | 14.55% | 1371.83 | 4.82% | 21.11 |

| Ceat Ltd. | 15678.00 | 2047.20 | 13.06% | 681.44 | 4.35% | 22.10 |

Key insights on JK Tyres & Industries Ltd.

- Pioneer and market leader in Truck and Bus Radial (TBR) technology. Strong dealer and distribution network across the country.

- Massive retail footprint backed by 650+ exclusive brand outlets pan-India.

- Direct beneficiary of India’s highway expansion and rising commercial freight.

- Aggressive product pivot toward high-margin luxury SUV and EV tyres.

- Strong export hedge anchored by its highly profitable Mexican subsidiary.

- Sticky OEM relationships enhanced by proprietary ‘Smart Tyre’ digital sensors.

- Improving balance sheet driven by resilient double-digit operating margins.

Recent financial performance of JK Tyre Ltd. for Q4 FY26

| Metric | Q4 FY25 | Q3 FY26 | Q4 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 3758.60 | 4222.96 | 4223.44 | 0.01% | 12.37% |

| EBITDA (₹ Cr.) | 363.09 | 570.79 | 537.07 | -5.91% | 47.92% |

| EBITDA Margin (%) | 9.66% | 13.52% | 12.72% | -80 bps | 306 bps |

| PAT (₹ Cr.) | 102.43 | 209.05 | 187.76 | -10.18% | 83.31% |

| PAT Margin (%) | 2.73% | 4.95% | 4.45% | -50 bps | 172 bps |

| Adjusted EPS (₹) | 3.61 | 7.21 | 6.17 | -14.42% | 70.91% |

JK Tyres & Industries Ltd. financial update (Q4 FY26)

Financial performance

- Revenue grew 11.1% YoY to ₹16,327 crore in FY26, driven by strong demand across commercial and passenger radial segments.

- EBITDA surged 18.1% YoY to ₹1,943 crore, supported by operational efficiencies and an improved product mix.

- EBITDA margin expanded 70 bps YoY to 11.9%, reflecting stronger bottom-line profitability.

- PAT increased 52.5% YoY to ₹776 crore, aided by robust operating performance and lower interest drag. .

- Return ratios remained strong, with ROE at 16.2% and ROCE at 15.5%, highlighting efficient capital deployment across expansions.

Business highlights

- The commercial and passenger radial business delivered strong growth, supported by healthy demand across logistics, infrastructure, and automobile replacement cycles.

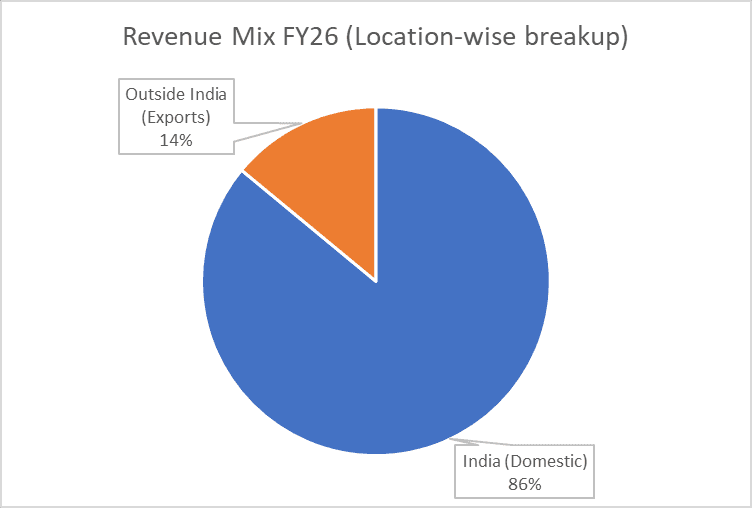

- Export contribution accounts for roughly 14-16% of revenue, with the company serving global customers across more than 100 countries.

- JK Tyre expanded its distribution network to over 6,000 dealers and added multiple exclusive retail brand touchpoints across India.

- The company continues to focus on premium products, export expansion, and higher-value radial segments to drive growth.

- A ₹4,980 crore phased capex program is underway to expand radial tyre capacity and improve overall operational efficiency.

Outlook

- Management expects healthy volume growth across its core radial segments, supported by sustained domestic infrastructure momentum and rising commercial fleet utilization.

- The ongoing premiumization strategy targets a significantly higher revenue contribution from 16-inch and above passenger tyres, aiming for steady EBITDA margin expansion toward 13–14% over the next two years

- Heavy commercial (TBR) and Off-The-Road (OTR) tyre volumes are projected to remain robust, driven by elevated government spending in road construction and mining activity.

- Aggressive scaling of dedicated Electric Vehicle (EV) tyres and tech-enabled TPMS fleet solutions is expected to increase realization per unit and unlock new high-margin market opportunities.

- Long-term growth remains firmly anchored by the formalization of Indian logistics, rising passenger vehicle density, expanding export reach across the Americas, and a deepening Tier-2 and Tier-3 retail network.

Recent Updates on JK Tyre & Industries Ltd.

- Continuous expansion of the premium passenger tyre portfolio.

- Strengthening distribution reach across Tier-2 and Tier-3 cities.

- Greenfield and brownfield capacity additions to meet upcoming demand.

- Increased focus on eco-friendly and EV-specific tyre variants.

- Expansion of the smart-tyre ecosystem and tech-driven fleet solutions .

Company valuation insights – JK Tyre & Industries Ltd.

JK Tyre is currently trading at a forward P/E of 15.5x FY26E, offering a reasonable entry point compared to its historical valuation bands. The stock has delivered a strong absolute return of 11.8% over the last one year, significantly outperforming the benchmark Nifty 50 at -4.5% during the same period.

The investment case for JK Tyre is supported by its pioneering position in the truck and bus radial industry, extensive distribution network, growing export footprint, and rising exposure to structural mobility and infrastructure themes. The company continues to solidify its market presence through its deep network of over 6,000 independent dealers and exclusive brand outlets across India. Its core passenger and commercial radial volumes are expected to remain robust, heavily supported by accelerating fleet utilization and highway development. Under its structured operational goals, management is targeting steady volume growth alongside margin expansion through product premiumization, improved operating leverage, and robust international market coverage. Additionally, the ongoing capacity expansions across passenger and commercial segments, including major expansion projects at the Banmore and Laksar facilities, along with a sharp focus on high-margin EV-specific tyres and digital fleet management systems, provide multiple levers for sustainable earnings growth. Supported by high brand recall and healthy return ratios, JK Tyre remains well-positioned to capitalize on India’s long-term automotive and logistics infrastructure growth story.

From a valuation perspective, valuing the company at 16x FY28E EPS of ₹32, we arrive at a 12-month target price of ₹512, implying an upside potential of approximately 24% from current levels. In the near term, we assign a 3-month target price of ₹440, indicating a more modest 7% upside. Going forward, a sustained re-rating will be driven by continued replacement demand, recovery in the commercial vehicle cycle, improving export volumes, and the company’s ability to sustain margin expansion through a favorable product mix and stable raw material costs.

Major risk factors affecting JK Tyre & Industries Ltd.

- Raw Material Risk: Natural rubber and crude derivative price volatility impacting margins.

- Competition Risk: Intense competition from established tyre industry players.

- Execution Risk: Committing capital and scaling major capacity expansions at Banmore and Laksar profitably.

- Infrastructure Slowdown Risk:Lower commercial vehicle and construction activity affecting fleet demand. .

- Distribution Expansion Risk: Maintaining dealer productivity and exclusive brand shop market penetration.

Technical analysis of JK Tyre & Industries Ltd.

JK Tyre is showing encouraging signs of a medium-term trend reversal, with the stock forming a well-defined inverse head and shoulders pattern and trading just below its neckline resistance. A decisive breakout above the neckline would confirm the bullish reversal pattern and could trigger a fresh round of momentum buying. The stock is currently trading above its 20-day, 50-day and 100-day EMAs, while it is on the verge of reclaiming its 200-day EMA, signalling improving price structure and strengthening medium-term trend dynamics. A sustained move above the neckline would reinforce the bullish setup and support our 12-month target price of ₹512.

Momentum indicators are gradually turning favourable. The MACD at 4.86 remains positive and is trading above its signal line, indicating improving bullish momentum and strengthening buying interest. The RSI at 60.79 reflects healthy buying participation while remaining below overbought territory, suggesting there is room for further upside. Additionally, the 21-day Relative RSI at 0.04 indicates that the stock has started outperforming the broader benchmark, reinforcing the improving relative strength.

Trend strength is still in the early stages of development, with the ADX at 18.05 indicating that the stock remains in a range-bound phase. However, a confirmed breakout above the inverse head and shoulders neckline could lead to a meaningful improvement in trend strength, with ADX expected to rise as buying momentum accelerates. A sustained move above ₹440 would confirm the breakout and could pave the way towards ₹512, our 12-month fundamental target. We recommend maintaining a stop-loss at ₹385 to manage downside risk.

- RSI: 60.79 (Healthy buying interest)

- ADX: 18.05 (Range-bound; likely to strengthen after breakout)

- MACD: 4.86 (Positive; above signal)

- Resistance: ₹440

- Support: ₹385

JK Tyre & Industries Ltd. stock recommendation

Current Stance: Buy, with a 12-month target price of ₹512 (24% upside), and a 3-month target of ₹440 (7% upside), based on a valuation of 16x FY28E EPS of ₹32,

Why buy now?

Strong volume demand across domestic commercial replacement networks, high-growth farm equipment segments, and the passenger vehicle upcycle provides steady long-term revenue visibility.

The company continues to solidify market share through its massive pan-India distribution pipeline of over 6,000 independent dealers and exclusive brand shops.

Strategic management initiatives target strong operational recovery and double-digit EBITDA margin expansion (projected at 13.0% by FY27) via structural product premiumization and improved asset utilization.

A well-timed ₹1,200 crore capital expenditure program focused on radial capacity additions at Banmore and Laksar ensures the company is equipped to address future high-margin volume demands.

Growing global export opportunities, strong international performance via its Mexican arm (JK Tornel), robust manufacturing capacity utilization above 88%, and exceptional domestic brand recall position the company to deliver highly sustainable earnings growth over the medium to long term

Portfolio fit

JK Tyre provides exposure to India's automotive upcycle, infrastructure expansion, and logistics growth themes through its strong presence in commercial radials, premium passenger tyres, and specialized off-road products. Backed by a deep distribution network, expanding export footprint, increasing share of higher-margin premium radial products, strategic capacity expansion initiatives at the Banmore and Laksar facilities, and strong brand recognition, the company is well positioned to benefit from rising investments in logistics networks, fleet commercialization, and electric mobility transit, making it a suitable addition to growth-oriented portfolios.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebJK Tyre & Industries Ltd.: Budget 2026-27 opportunities

- National Highways & Logistics Infrastructure: Increased freight movement and fleet utilization driving robust commercial tyre replacement demand.

- Rural Push & Agricultural Allocation: Revival in rural income boosting tractor and farm equipment tyre volumes across OEM and replacement markets.

- Urbanization & EV Mobility Incentives: Accelerating demand for premium passenger radials and specialized electric vehicle tyre segments.

- Manufacturing & Mining Capex Expansion: Sustained infrastructure projects fueling solid demand for heavy-duty, extreme-durability Off-The-Road (OTR) tyres.

- Make in India & Export Promotion: Supporting domestic capacity building and enhancing competitive global positioning despite international trade headwinds.

Final thoughts

JK Tyre & Industries Limited stands at the intersection of several powerful long-term themes: logistics modernization, highway expansion, infrastructure spending, and automotive premiumization. With a strong brand, extensive distribution network, pioneering radial product portfolio, and a growing presence in smart mobility solutions, the company is well-positioned to capitalize on India’s evolving transportation ecosystem.

For investors seeking exposure to India’s infrastructure and automotive growth story through a scalable branded business, JK Tyre offers a compelling combination of market leadership, volume growth visibility, and long-term compounding potential.