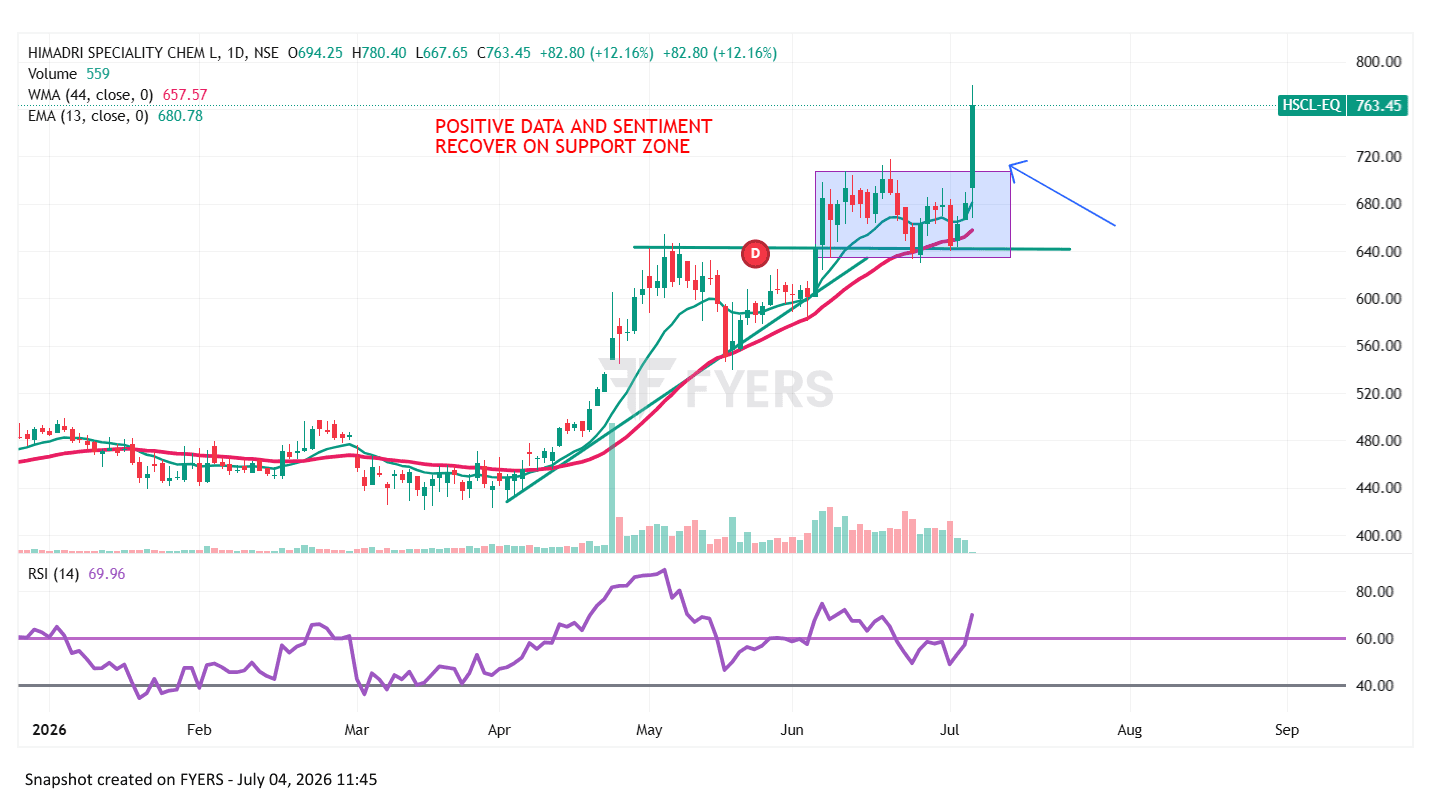

Himadri Speciality Chemical Ltd. (HSCL) – SWOT Analysis

$HSCL Strengths Market leader in coal tar pitch, specialty carbon black, naphthalene, and carbon materials in India with a diversified specialty chemicals portfolio. Strong financial performance with healthy profitability, ROCE of around 22%, improving operating margins, and consistent earnings growth. Strong R&D capabilities and transition toward high-value specialty products instead of commodity chemicals. Strategic entry into EV battery materials, including anode materials and silicon-carbon technology, creating a long-term growth avenue. Growing export presence with customers across multiple countries and diversified end-user industries. Weaknesses Core business remains linked to coal tar derivatives, making earnings partially dependent on steel and aluminium industry demand. Raw material prices can be volatile, affecting operating margins. Valuation has become relatively expensive after the strong rally, leaving limited room for disappointment. Recent decline in promoter shareholding is a point investors should monitor. Opportunities Rising global demand for EV batteries, energy storage systems, and advanced carbon materials. Commercialization of anode materials and silicon-carbon technology can significantly increase revenue over the next few years. China+1 sourcing strategy creates export opportunities for Indian specialty chemical manufacturers. Capacity expansion in specialty carbon black and battery materials can improve market share and profitability. Increasing infrastructure and automotive demand supports long-term growth in specialty chemicals. Threats Cyclical demand from steel, aluminium, and automobile sectors. Competition from global specialty chemical and battery material manufacturers, especially Chinese producers. Environmental regulations and compliance costs may increase operating expenses. Currency fluctuations and global economic slowdown could impact export demand. Investment View Positives