$OLECTRA Olectra Greentech Q4 FY26 Results show a very strong performance

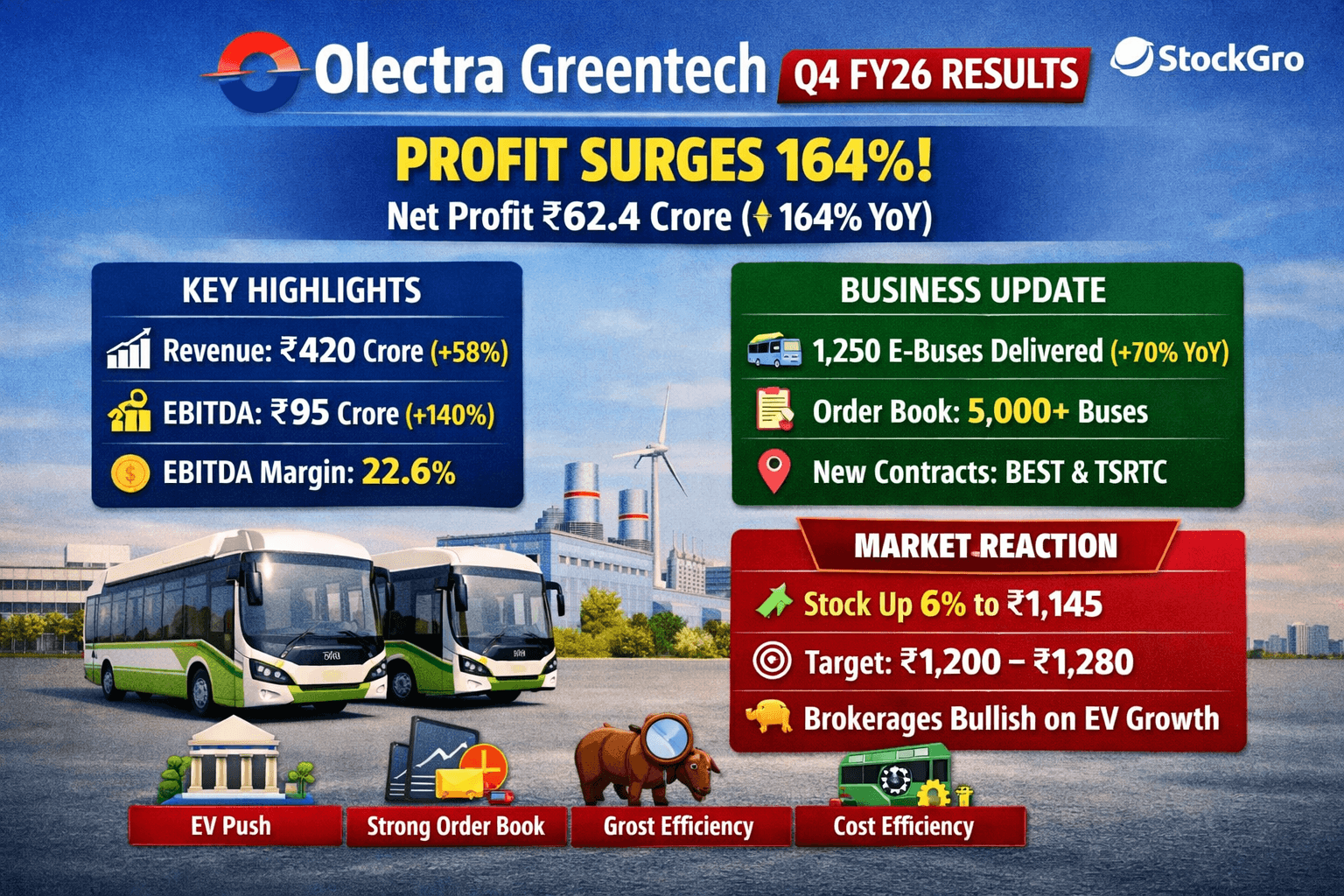

Olectra Greentech Q4 FY26 Results show a very strong performance, with profits surging on the back of higher demand for electric buses and improved margins. ⚡ Financial Highlights Net Profit: ₹62.4 crore (↑ 164% YoY vs. ₹23.6 crore last year) Revenue from Operations: ₹420 crore (↑ 58% YoY) EBITDA: ₹95 crore (↑ 140% YoY) EBITDA Margin: 22.6% (vs. 15.2% last year) EPS: ₹5.2 (vs. ₹2.0 last year) 🚌 Business Performance Electric Bus Deliveries: 1,250 units in Q4 (↑ 70% YoY) Order Book: Over 5,000 buses pending delivery across multiple state transport undertakings. New Contracts: Secured supply agreements with BEST (Mumbai) and TSRTC (Telangana). Expansion: Plans to scale manufacturing capacity to 3,000 buses annually by FY27. 📈 Market Reaction Share Price: Rose ~6% to ₹1,145 after results. Brokerages: Motilal Oswal: Target ₹1,250, maintain Buy. ICICI Direct: Target ₹1,200, citing strong order book. HDFC Securities: Target ₹1,280, bullish on EV adoption. 🔑 Key Drivers Government EV push and subsidies. Rising demand from state transport corporations. Improved cost efficiency and economies of scale.