$APLAPOLLO

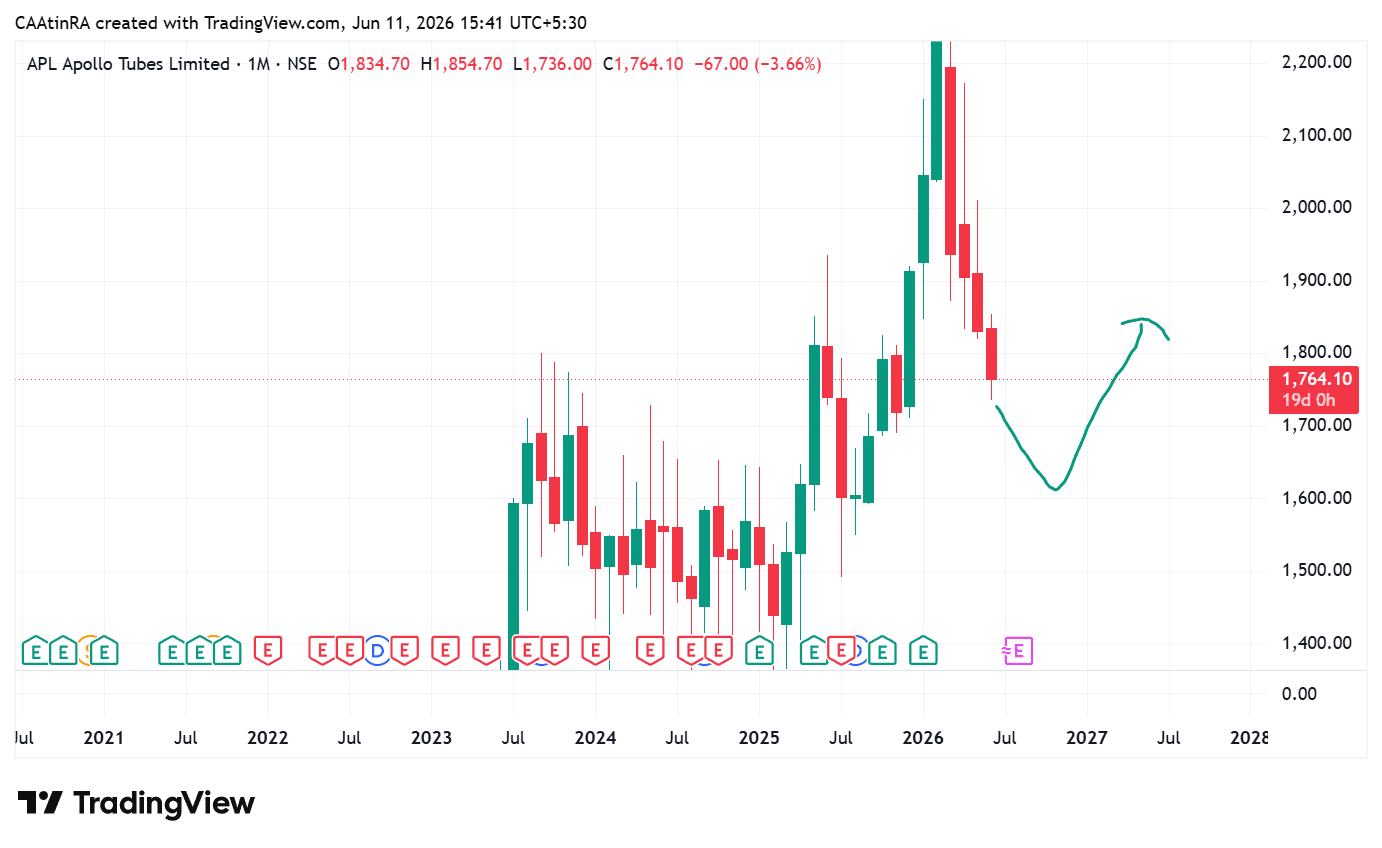

$APLAPOLLO APL Apollo is India's leading structural steel tube manufacturer and continues to gain market share through product innovation, strong distribution, and capacity expansion. The company remains a proxy on India's infrastructure, housing, warehousing, solar, and industrial capex growth. Key Positives ✅ Market Leadership Largest branded structural steel tube player in India. Strong dealer network and brand recall. Premium products provide better margins than commodity steel pipes. ✅ Strong Volume Growth FY26 sales volume grew 11% to 3.49 million tonnes. Management is targeting 15–20% volume growth in FY27. ✅ Margin Improvement EBITDA per tonne improved above ₹5,500 in recent quarters. Profit growth is significantly higher than revenue growth, indicating operating leverage. ✅ Strong Balance Sheet Net cash position and virtually zero working-capital model. High ROCE compared to most steel-sector peers. Key Risks ⚠️ Steel price volatility can impact margins. ⚠️ Large capacity additions by industry players may increase competition. ⚠️ Future growth depends heavily on maintaining high utilization of new capacities. Market participants closely track utilization levels because they directly affect margins and return ratios.