$AXISBANK

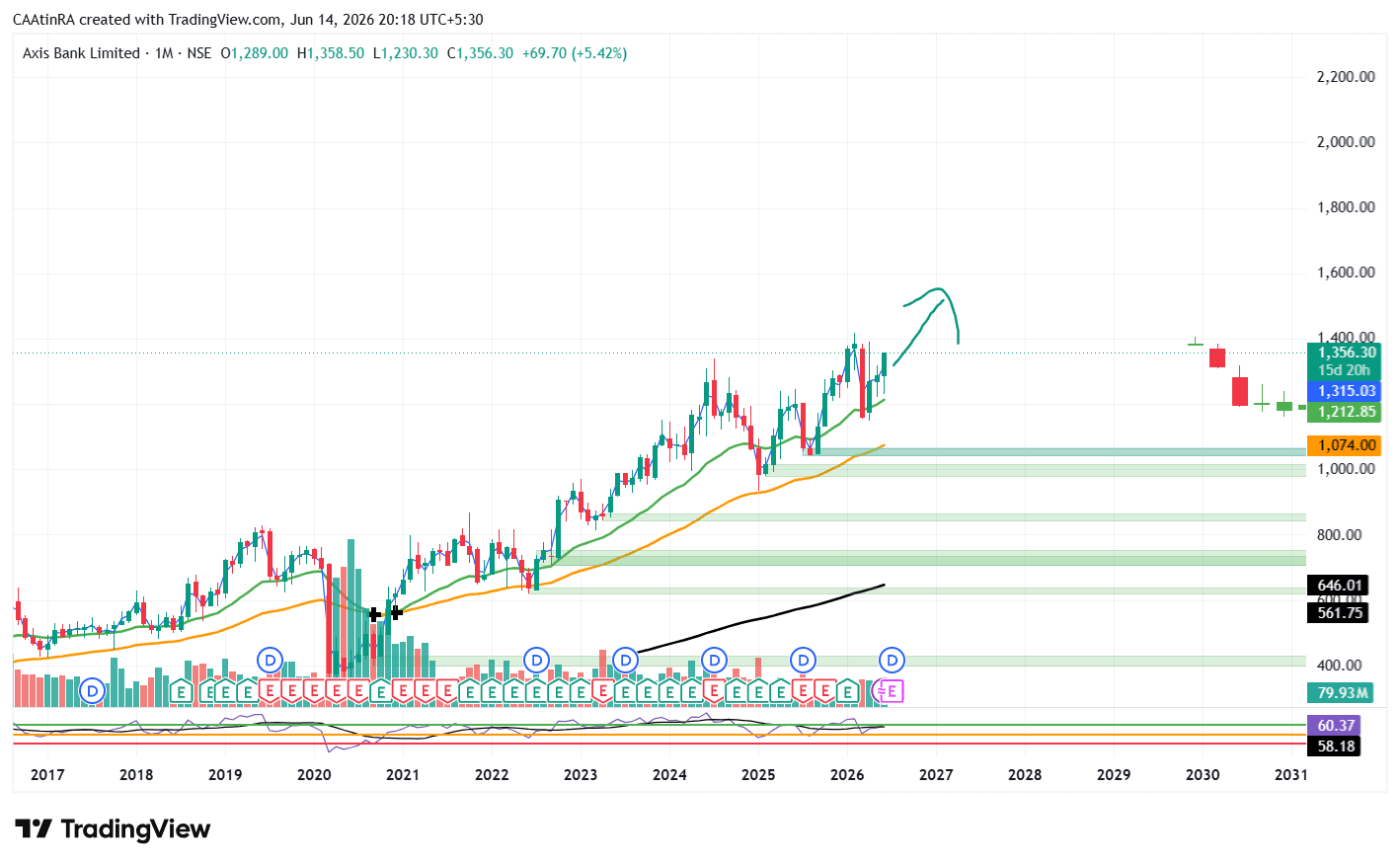

$AXISBANK Axis Bank is India's third-largest private sector bank and remains one of the key beneficiaries of India's long-term credit growth story. Positives ✅ Strong Loan Growth Retail, SME and corporate lending continue to support business growth. The bank has been steadily gaining market share in several lending segments. ✅ Improving Asset Quality Gross NPA and Net NPA levels have improved significantly over the last few years. Lower credit costs support profitability. ✅ Citibank Consumer Business Acquisition Integration benefits are gradually flowing into earnings through cross-selling opportunities and a larger customer base. ✅ Digital Banking Strength Strong focus on digital platforms, payments and wealth management businesses helps diversify revenue streams. Risks ⚠️ Banking stocks remain sensitive to RBI policy changes and interest-rate cycles. ⚠️ Any slowdown in credit growth or rise in bad loans could impact valuations. ⚠️ Margin pressure may emerge if deposit costs rise faster than loan yields. Technical View Long-Term Trend: Bullish The stock continues to trade within a long-term uptrend structure. Institutional ownership remains strong. Higher highs and higher lows on the weekly chart indicate positive momentum. Key Zones Immediate Support: ₹1,150–1,180 Strong Support: ₹1,080–1,120 Resistance: ₹1,300–1,350 Major Breakout Zone: Above ₹1,350 Fundamental View ROA and ROE continue to improve. CASA franchise remains strong. Credit growth outlook remains healthy due to India's expanding economy. Valuation is reasonable compared with many private-sector peers.