$BIKAJI

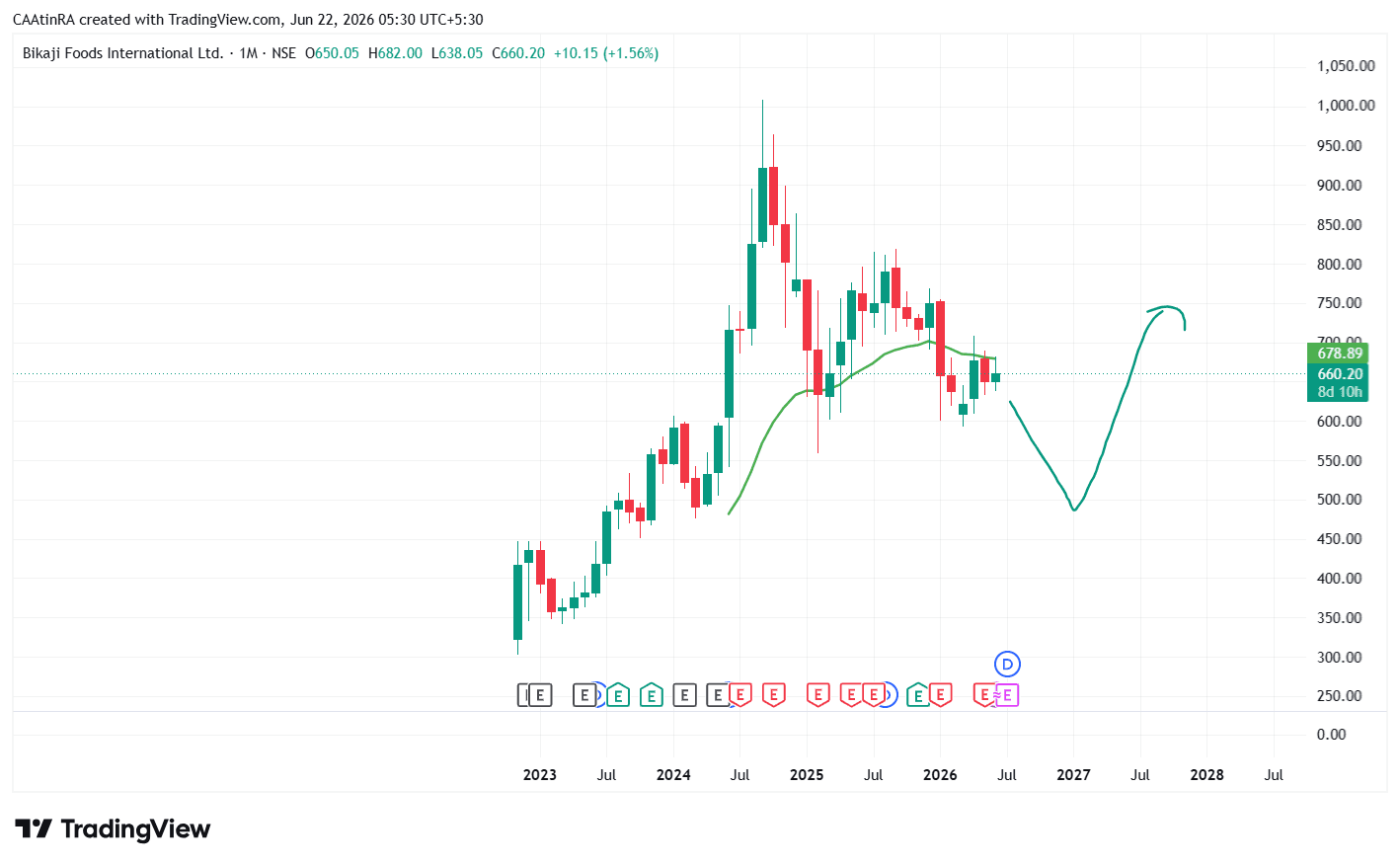

$BIKAJI Investment Thesis Bikaji is one of India's fastest-growing branded ethnic snacks companies, competing with players such as Haldiram's, Prataap Snacks and Balaji Wafers. The company is benefiting from the long-term shift from unorganized snacks to branded packaged foods. Recent Financial Performance Q4 FY26 results were strong on the revenue front: Revenue grew around 18% YoY. Volume growth remained robust at over 16%. PAT increased nearly 40% YoY. Gross margins improved due to favorable raw material costs and better operating leverage. For FY26: Revenue growth: 14.4% PAT growth: 31% EBITDA margin improved to around 13.7%. Positives 1. Strong Brand in Ethnic Snacks Bikaji enjoys strong brand recall, particularly in North and West India, where traditional namkeen and bhujia categories continue to grow. 2. Volume-Led Growth Unlike many FMCG companies relying mainly on price hikes, Bikaji's growth is currently volume-driven, which is generally a healthier indicator. Volume growth in Q4 FY26 exceeded 16%. 3. Margin Expansion Opportunity Management expects operating leverage benefits from new warehouses, distribution expansion, and higher capacity utilization. 4. Large Growth Runway The branded snacks market in India continues to grow faster than overall FMCG, creating a long runway for organized players. Management is targeting double-digit volume growth in FY27.