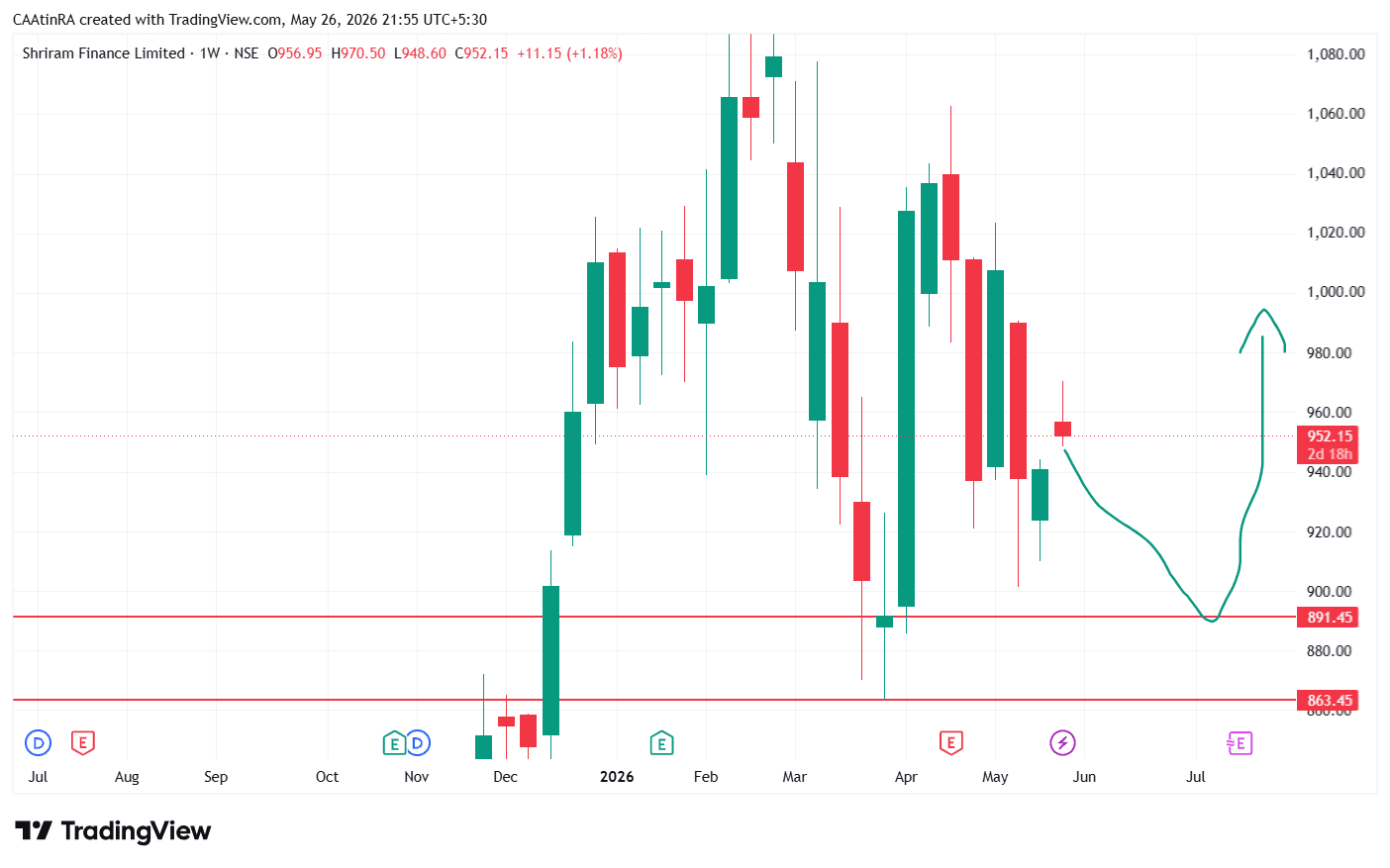

$SHRIRAMFIN

$SHRIRAMFIN Shriram Finance Limited is one of the strongest retail-focused NBFCs in India, with leadership in commercial vehicle finance, MSME lending, two-wheelers and rural lending. The stock is generally viewed as a “growth + value” play because it combines double-digit AUM growth with relatively moderate valuation multiples compared to larger private banks and premium NBFCs. Business snapshot AUM crossed about ₹3 lakh crore in FY26, growing nearly 15% YoY. Q4 FY26 PAT grew ~41% YoY to around ₹3,020 crore. Net NPA improved to ~2.33%, indicating improving asset quality. Dividend for FY26 totals ₹10.8/share. Positives for the stock 1. Strong retail franchise Shriram has decades-old dominance in used CV financing and semi-urban/rural lending. This customer base is difficult for banks to penetrate. 2. Improving asset quality GNPA and NNPA trends have been steadily improving after merger integration. Credit cost normalization supports profitability. 3. Earnings growth visibility Management continues guiding for mid-teen loan growth with margin recovery as surplus liquidity gets deployed. 4. Funding diversification The company is expanding overseas borrowing avenues, including yen funding discussions, which may gradually reduce cost of funds. 5. Valuation still reasonable Compared with high-quality NBFC peers, Shriram Finance often trades at lower P/B multiples despite: ROA near 3% Strong ROE High retail granularity Improving balance sheet This is why many brokerages continue maintaining “Buy” ratings despite recent volatility. Risks to watch 1. Cyclical business exposure 2. Growth moderation Recent quarters showed slower-than-guided AUM growth. Some analysts believe management prioritized margins over aggressive expansion. 3. Interest-rate sensitivity NBFC margins can compress if borrowing costs remain elevated for long. 4. Rural stress risk Weak monsoons, fuel inflation, or transport-sector slowdown can affect collections.