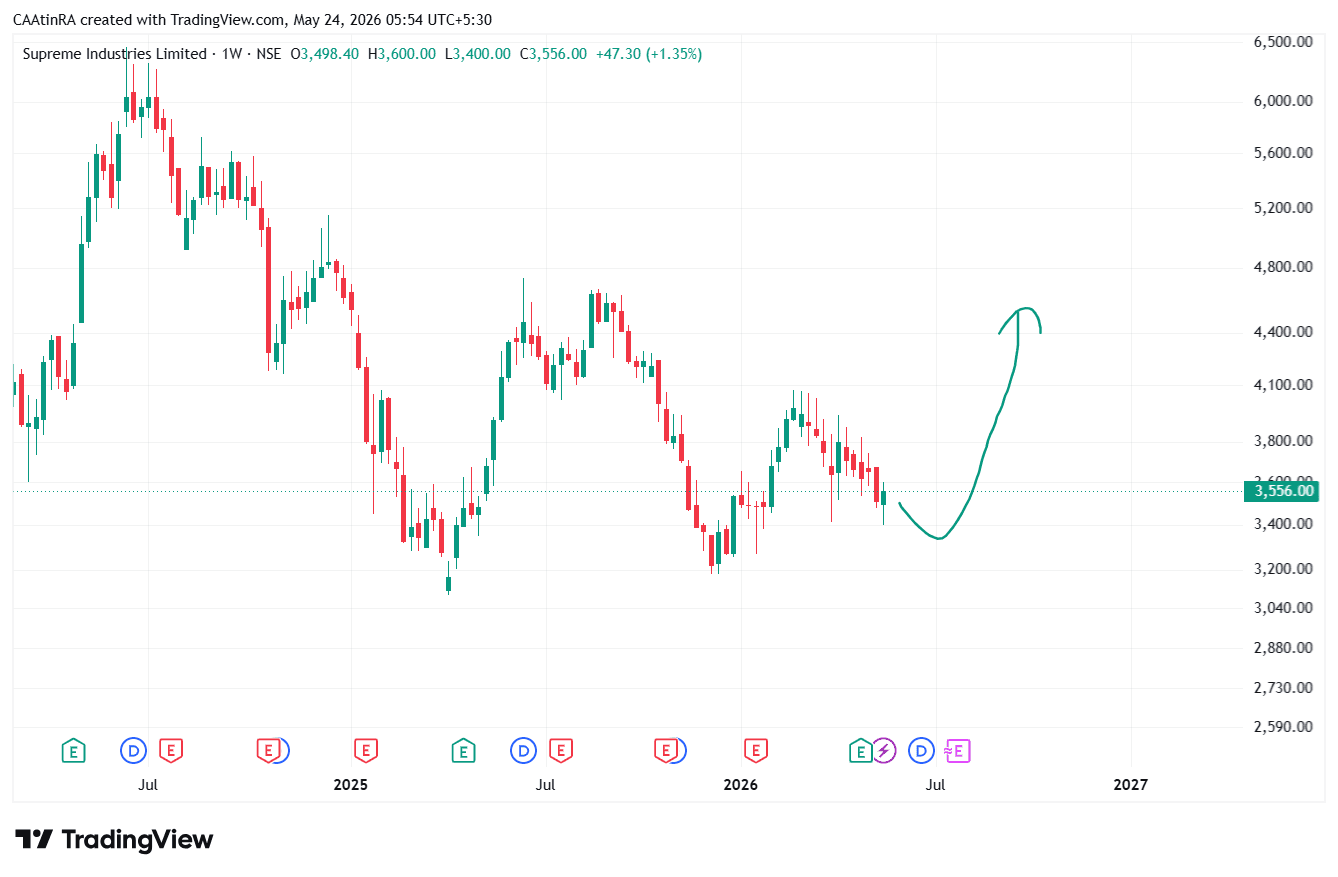

$SUPREMEIND

$SUPREMEIND Business Overview Supreme Industries is one of India’s largest plastic processing companies with leadership across: Plastic piping systems Packaging products Consumer products Industrial components The company benefits from: Strong dealer/distribution network Brand leadership in pipes & fittings Housing, irrigation and infrastructure demand Consistent dividend history Its piping business remains the key growth driver. Fundamental Analysis Positives Strong balance sheet with low debt Healthy ROCE profile above 20% in recent periods Market leader in plastic piping Capacity expansion underway for future growth Q4FY26 numbers were strong: Revenue up 17% YoY PAT up 48% YoY EBITDA margins improved sharply Concerns PVC raw material volatility impacts margins heavily Demand slowdown in industrial and export segments Valuations remain expensive compared to historical averages Growth moderation seen in FY26 guidance Valuation Current valuation metrics remain rich: P/E around 46–49x Sector P/E materially lower than company valuation This suggests the market is pricing in: Long-term leadership Strong future demand recovery Margin normalization But near-term earnings volatility can keep the stock volatile.