$SWIGGY

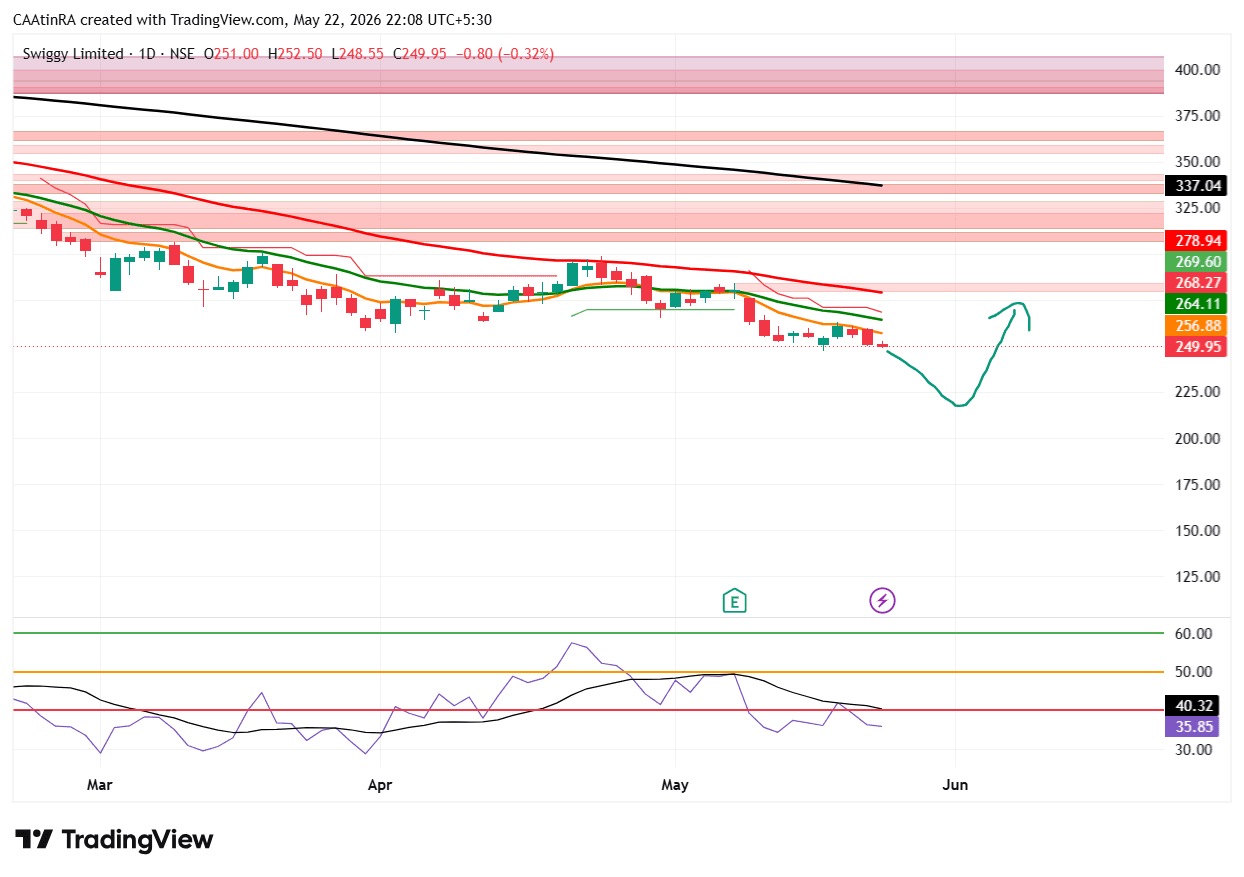

$SWIGGY Swiggy is currently trading in a phase where the market is balancing strong revenue growth against continued profitability concerns. The company’s food delivery business is improving steadily, but aggressive competition in quick commerce (Instamart) is keeping investor sentiment volatile. Business Overview Swiggy operates across: Food Delivery Instamart (Quick Commerce) Dineout Genie & logistics services The major long-term growth driver remains India’s expanding quick-commerce and online food delivery ecosystem. Fundamental Analysis Positives 1. Strong Revenue Growth Swiggy reported around 45% YoY revenue growth in Q4 FY26, showing strong user expansion and order growth. 2. Food Delivery Margins Improving The core food delivery business delivered its strongest growth in nearly four years and crossed ₹1,000 crore adjusted EBITDA annually. 3. Expanding User Base Monthly transacting users increased strongly, reflecting continued adoption in tier-2 and tier-3 cities. 4. Huge Long-Term Market Opportunity India’s online grocery and food delivery penetration is still relatively low compared with global markets, leaving significant room for expansion. Concerns / Risks 1. Profitability Still Weak Despite revenue growth, Swiggy continues to report large losses because of: Heavy discounting Dark store expansion Intense quick-commerce competition 2. Instamart Competition Competition from: Blinkit Zepto Amazon Flipkart is pressuring margins and market share. Reuters noted that Instamart growth lagged Blinkit recently. 3. Expensive Valuation for a Loss-Making Company The market is still valuing Swiggy on future growth potential rather than earnings. That means: High volatility Sharp corrections after results Sentiment-driven movement 4. Regulatory & Ownership Issues Swiggy recently failed to obtain approval for changes needed to classify itself as an Indian-owned company.