$ASHOKLEY Ashok Leyland reported its highest-ever quarterly results in Q4 FY26

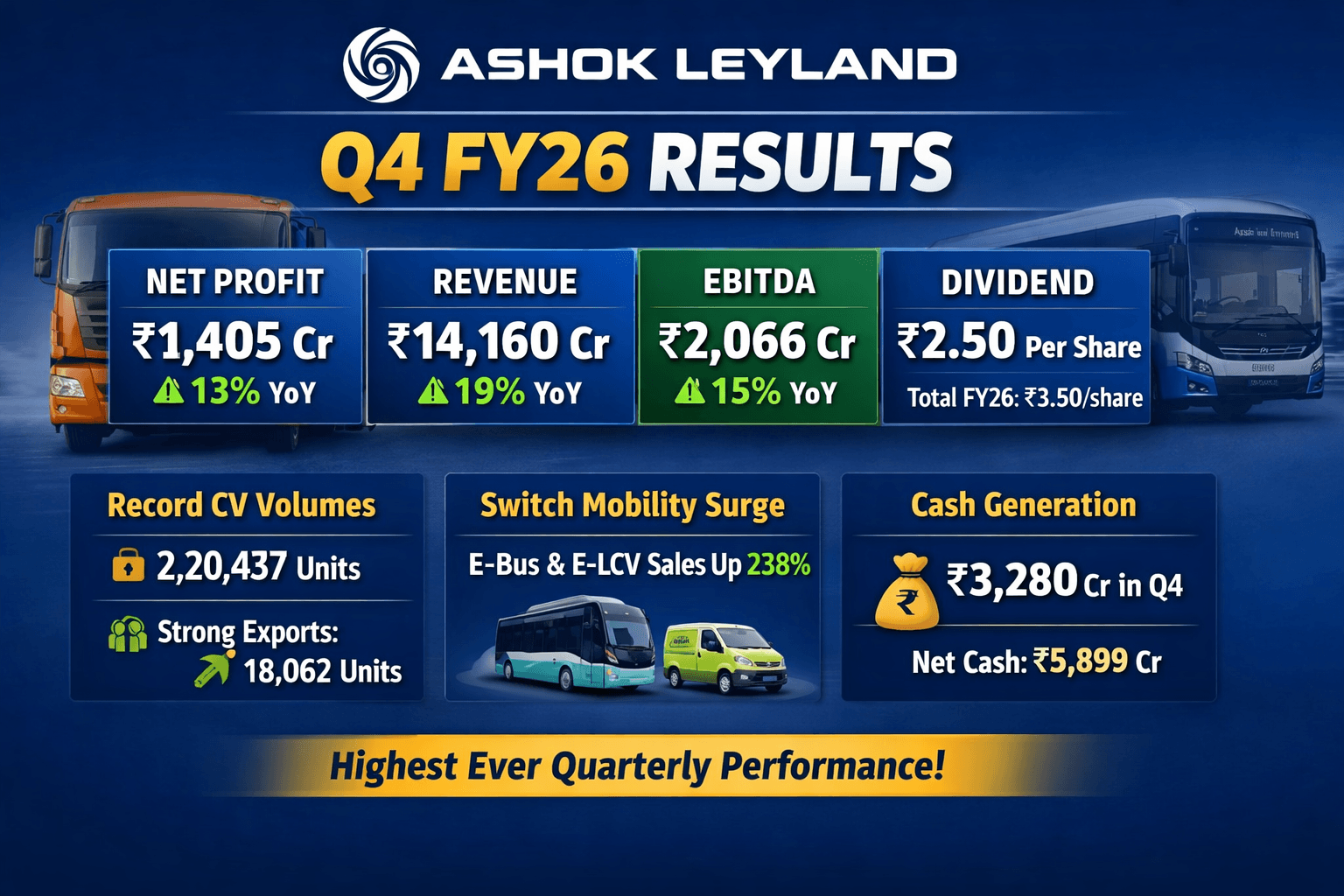

Ashok Leyland reported its highest-ever quarterly results in Q4 FY26, with net profit rising 13% YoY to ₹1,405 crore and revenue surging 19% to ₹14,160 crore, driven by record commercial vehicle volumes, strong exports, and growth in electric mobility. The company also declared a dividend of ₹2.50/share, taking the FY26 payout to ₹3.50/share. 📊 Ashok Leyland Q4 FY26 Highlights Net Profit (PAT): ₹1,405 crore (↑13% YoY) Revenue: ₹14,160 crore (↑19% YoY) EBITDA: ₹2,066 crore (↑15% YoY) Cash Generation: ₹3,280 crore in Q4 Dividend: Second interim dividend of ₹2.50/share; total FY26 dividend ₹3.50/share Volumes: Total CV volumes: 220,437 units (record high, surpassing FY19 peak) LCV volumes: 74,322 units (new record) Exports: 18,082 units (↑18.5% YoY) Electric Mobility (Switch Mobility): E-bus volumes ↑238% to 1,530 units E-LCV volumes ↑56% to 1,606 units Revenue doubled to ₹1,807 crore; turned profitable with PAT ₹104 crore 📌 Full-Year FY26 Performance Annual Revenue: ₹44,007 crore (↑14% YoY) Annual PAT: ₹3,566 crore (↑8% YoY) despite a one-time labour code charge of ₹308 crore Annual EBITDA: ₹5,732 crore (margin 13%) Net Cash Reserves: ₹5,899 crore (up from ₹4,242 crore in FY25) ⚠️ Market Reaction Despite strong earnings, Ashok Leyland’s share price fell ~3% to ₹158.69 on May 29, 2026, as brokerages flagged near-term uncertainty in truck demand due to rising fuel and commodity costs. Brokerages like Jefferies maintained a “Hold” rating, citing margin pressures and weak visibility in demand. 📌 Key Takeaways Strengths: Record CV volumes, strong exports, electric mobility turnaround, robust cash reserves. Challenges: Rising fuel/commodity costs, margin pressures, cautious outlook from brokerages. Investor Note: Dividend payout and strong fundamentals support long-term confidence, but near-term volatility in demand may weigh on stock performance.